-

Home

-

Maritime Training

- elnavi

elnavi

“Windea Leibniz” is ready to boost offshore wind power expansion in the Baltic and North Sea

On 4 February 2023, BSM managed Service Operation Vessel (SOV) “Windea Leibniz” finished an extensive upgrade at Ulstein Shipyard in Norway. With an increase of cabins from 60 to over 80, the vessel has transitioned from an SOV to a Commissioning Service Operation Vessel (CSOV). Additionally, the ship received one extra pedestal on the stern for Baltic Sea operations to complement the existing pedestal for North Sea use. The upgrade expands the operational range of “Windea Leibniz” and makes her even more attractive for the offshore market.

The upgrade of “Windea Leibniz” was timed perfectly as European governments want to expand renewable energy capacities in the Baltic and North Sea. Last year the EU had a capacity of approximately 15 gigawatts (GW) in offshore wind power production. Germany alone is aiming to double their capacities by 2030. According to the German government, this equals an expansion of offshore wind energy to at least 30 GW by 2030, with at least 40 GW of installed capacity by 2035 and at least 70 GW by 2045.

Supporting the expansion of renewable energy sources

“Offshore wind is an essential part for the success and the transformation of the energy sector towards sustainable and green solutions. The upgrade makes ‘Windea Leibniz’ even more attractive for the market,” says Matthias Mueller, Managing Director of shipowner Bernhard Schulte Offshore.

“Windea Leibniz" is now ready to support the planned offshore wind power expansion in Northern Europe. The ultra-modern SOV was built in 2017 at Ulstein Shipyard for Bernhard Schulte Offshore to efficiently service offshore wind farms in the North Sea. The vessel functions as a reliable and environmentally sound platform for wind farm operations and maintenance support, technician accommodation and transport, and the provision of safe and reliable access to offshore installations.

50% increase of accommodation capacities

The upgrade included a 50% increase of accommodation capacities on board. Therefore, extensive reconstruction measures including shifting of the changing/drying rooms, conference rooms and day rooms were executed. In total the cabin capacity was increased from 63 to 81 cabins. Now “Windea Leibniz” can accommodate up to 85 technical staff for wind farms, service personnel and crew.

The second major milestone was the installation of a new height-adjustable pedestal for the motion compensating gangway, making the vessel more flexible in offshore wind farms. Now the gangway can operate in a range between 17.5 metres and 23 metres height above waterline when fully extended.

More flexibility for deployment in different wind farm markets

The third milestone focussed on the installation of a second pedestal for the gangway at stern. It enables “Windea Leibniz” to also sail in offshore wind parks in the Baltic Sea where service platforms are generally lower located than in the North Sea.

Rainer Mueller, Captain on the “Windea Leibniz” says, "With the two new pedestals, we are more flexible when approaching the service platforms for the wind turbines. There is no uniform standard for the height of the platforms in North Sea wind farms. After the yard stay, we can now vary with the height of our gangway. With the Baltic pedestal at stern, we can easily switch our gangway from the North Sea height to the lower Baltic Sea height, which makes us even more flexible when working in different wind farm regions. The new cabins allow us to accommodate more technicians on board. All this really makes ‘Windea Leibniz’ the new it-girl on the CSOV market."

Technical Specification "Windea Leibniz"

Length: 88 m

Beam: 18 m

Dead weight: 3150 tonnes

Draught (max): 6.4 m

Speed (max): 13.5 kn

Accommodation: 85 POB

Deck area: 380 sqm

About Bernhard Schulte Shipmanagement

Bernhard Schulte Shipmanagement (BSM) is an integrated maritime solutions provider. Managing a fleet of over 650 vessels, more than 20,000 seafarers and 2,000 shore-based employees enable the delivery of safe, reliable and efficient ship management services through a network of 11 ship management centres, 25 crew service centres and four wholly owned maritime training centres across the world. Alongside comprehensive ship management services, BSM offers a suite of complementary maritime solutions that are customised to meet individual customer requirements. As a member of the Schulte Group, BSM benefits from its 140+ years of experience in the shipping industry.

www.bs-shipmanagement.com

About Bernhard Schulte Offshore

Bernhard Schulte Offshore (BS Offshore) is the offshore unit of the renowned international shipping organisation Schulte Group. The company is an asset provider to the offshore wind industry providing bespoke vessels to fulfil the requirements of its clients, based on long-term charters. In addition, part of the existing fleet of Tier-1 Service Operation Vessels (SOV) is available for short-term needs. BS Offshore is a pioneer in offshore wind and built the first SOV without steps in 2015, enabling technicians to take spare parts with them from below deck to the wind turbine via a motion compensated gangway by use of an electrical trolley.

www.bs-offshore.com

Image1: “Windea Leibniz” at Ulstein Shipyard in Norway. ©BSM/Matthias Giebichenstein

image2: Installation of the new height-adjustable pedestal with 32 tonnes of weight. ©BSM

ELNAVI Newsletter

More information: ELNAVI,

19, Aristidou str., Piraeus 185 31,

Tel.: +30 210 45.22.100, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

A Look Into the Greek Maritime Fleet

Rebecca Galanopoulos Jones, Senior Content Analyst, highlights the Greek fleet breakdown by vessel type, top owning nations, S&P transactions, top Greek owners, CII distribution and the most valuable Greek vessels.

To mark the start of Capital Link Annual Greek Shipping Forum this week, we take a look at the Greek Maritime fleet using VesselsValue data. The infographic highlights the Greek fleet breakdown by vessel type, top owning nations, S&P transactions, top Greek owners, CII distribution and the most valuable Greek vessels.

Greek Fleet Breakdown

Bulkers are the most popular vessels within the Greek fleet, with a total of 2,272 vessels, followed by Tankers with 1,450 vessels and Containers with 430 ships. Tankers are the most valuable sector for Greece, worth USD 61.03 bil. This sector has recently seen extraordinary increases in values, which have hit 13 year highs over the last year. The price of a 15 year old Aframax of 110,000 DWT has surged by c.144% year on year from USD 16.17 mil to USD 39.43 mil. This is due to improved demand fundamentals and increased opportunities that have resulted from the ongoing conflict between the Ukraine and Russia. Despite a relatively small fleet of 127 vessels, soaring global demand for LNG has sent the value of this fleet sky high, with the fleet value for LNG carriers at USD 30.50 bil.

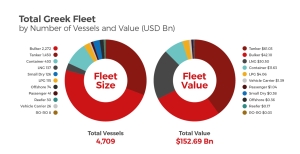

Greece Among Top Owning Nations

Of the top owning nations, the Greek fleet ranks third globally. This is both in number of vessels and total value, comprising of 4,709 vessels live and on order and a total value USD 152.69 bil. Overall, Japan tops the total value list with a fleet worth USD 193.64 bil, and China ranks first in terms vessel numbers with a fleet of 7,114 ships.

Greek S&P

In terms of S&P, Greece was the second top seller of secondhand vessels in 2022, with 428 vessels sold and a total value of USD 11.7 bil. Greece came behind China who sold 532 ships, receiving USD 12.93 bil. Greece was also the second biggest spender last year, splashing out USD 9.77 bil on a total of 376 vessels. Once again, Greece trailed behind China who spent an impressive USD 14.92 bil on 542 vessels. The UAE ranked third with USD 5.14 bil spent on 271 vessels.

Greek Beneficial Owners

Maran Gas Maritime, the LNG arm of the Angelicoussis Group, is ranked first in a list of the top five Greek owners with a fleet value of USD 8.01 bil. Additionally, their fleet consists of 22 live vessels and a further 12 on order. Thenamaris have the largest fleet with 95 vessels both live and on order and a total value of USD 5.24 bil. Tankers make up the majority of their trading fleet, accounting for 60% while the remainder consists of Bulkers, Containers, LNG and LNG carriers. Maran Tankers, also part of the Angelicoussis Group, came in third with a value of USD 4.62 bil and 56 vessels, followed by Minerva Maritime with a total value of USD 4.52 bil and 78 vessels. New York listed Tsakos Energy Navigation is ranked fifth with a value of USD 4.1 bil and consists of 68 vessels.

Estimated CII Distribution of Greek Fleet

Decarbonisation is an increasingly high priority to the Greek Shipping community; a large proportion of the Greek owned fleet ranks highly in the new mandatory energy efficiency ratings from the International Maritime Organisation (IMO). Over a quarter of the fleet have achieved an estimated CII rating of ‘A’, and 64% of the fleet have received an estimated rating between A-C.

Most Valuable Greek Vessels

The most valuable Greek owned cargo vessel is the recently delivered Clean Copano (199,830 CBM, Jul 2022, Hyundai Heavy Ind). Owned by Dynagas, this Large LNG carrier is valued at USD 286.11 mil. In the Ferry sector, the most valuable vessel is the Blue Star Patmos, owned Ropax Blue Star Ferries (18,498 GT, June 2012, Daewoo) and valued at USD 63.28 mil.

ELNAVI Newsletter

More information: ELNAVI,

19, Aristidou str., Piraeus 185 31,

Tel.: +30 210 45.22.100, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

With the participation of almost all IG P&I Clubs and after 2 years of pandemic the Piraeus Marine Club (PMC) organised the 22nd International P&I Conference which was chaired by Mr. Lou Kollakis, Honorary Chairman of Chartworld Shipping.

Opening addresses were delivered by Mr. Mr. George Alexandratos - General Manager of Apollonia Lines S.A - Chairman of the BoD of the PMC and Ms. Maria Prevezanou - Director of Evmar Marine Services Ltd. - Treasurer of the BoD of the PMC / Organiser of the Conference.

The following topics were discussed:

- Are further club mergers inevitable? Whose interests do they really serve?

- Is it time for clubs to reassess their portfolios, particularly as to asset class selection, given the volatility in the capital market?

- Expanding sanctions regimes implemented by carious countries and supranational entities over recent years have created both complexity and confusion for the shipping industry and Club’s perspective on this issue.

- Pool claims peaked from 2018 into 2021 whilst 2022 appears to be benign. Can the current pooling systems and especially Hydra and the Group’s excess of loss reinsurance address the larger pool claims?

Speakers of the first panel were: Ms. Dorothea Ioannou, CEO The American Club,

Mr. Jeremy Grose Chief Executive The Standard Club and Mr. Sean Geraghty Regional Director of Greece Thomas Miller P&I Ltd (UK Club).

The co-ordinator of the panel Mr. George Gourdomichalis asked the speakers to comment on the latest P&I developments.

Mr. Jeremy Grose from The Standard Club referred to the recent merger of North of England P&I and Standard Club and commented on the reasons that dictated the successful completion of the deal such as financial compatibility and business philosophy.

Mr. Sean Geraghty from Thomas Miller P&I Club told that is not interested in merging with another Club of minor or bigger scale. He does not see that there is a strong momentum for mergers and acquisitions and specific interest under the current market conditions.

The speakers also referred to the elements of the P&I Clubs administration costs such as claims & operational management to support members and provide the service that are looking for.

Mrs. Dorothea Ioannou CEO of The American Club pointed out that there are very particular circumstances in order to proceed to a merger and joint venture which depend on the similarities between two clubs including common retention program and risk profile.

At the end of the day the clubs compete on the service that they offer to the members and the expertise of their personnel.

Mr. Gourdomichalis concluded that mergers are possible to happen in this turbulent environment and aim at further investments and better service.

The second panel included the following speakers: Mr. Stephen Martin Executive Chairman of Steamship Insurance Management Services, Mr. Ludvig Nyhlen Area Manager Team Piraeus The Swedish Club and Mr. Kjell-Ake Augustsson Senior Vice President, Head of Skuld Piraeus.

Mr. Ludvig Nyhlen from The Swedish Club told that one of the cornerstones of our investment policy is to protect the club’s capital and attract higher yield in the long term as well as constantly access the assets.

The speakers agreed that you have limited parameters for investments according to the solvency rules and the benefits/profits returns always to the members.

In the US marine insurance market according to Joe Hughes from The American Club the P&I Club has to comply with Risk Based Capital (RBC) authorities reporting quarterly and maintaining capital at a certain level based on the tonnage and the risk profile.

The following speakers Mr Mike Salthouse Global Director (Claims) North of England P&I Association Limited, Mr. Konstantinos Samaritis Divisional Director Britannia Steam Ship Insurance Association Limited, Mr. George Karas Managing Director Gard Greece, Mr. Ian Clarke Head of Claims & Regional Director (Hellas) West of England Insurance Services SA discussed the controversial issue of sanctions regimes.

Mr. Ian Clarke from West of England underlined that sanctions lead to a very confused environment. West of England is working closely with the US and EU authorities to ensure that no restrictions are imposed to members’.

Konstantinos Samaritis from Britannia noted that we encourage our members to exercise due diligence to identify sanctions’ red flag.

It is of paramount importance to identify quality of the cargo and that the destination to be absolute legitimate.

P&I Clubs should maintain assessment departments and carry out continuous training programs to comply the sanctions regimes.

George Karkas from Gard outlined that you always have to think what will happen during the adventure from the port of loading until the port of discharge.

George Gourdomichalis commented that there is no safe way to comply with sanctions.

Mike Salthouse from NoE P&I Club mentioned that the issue of sanctions is notably complex.

In conclusion sanctions are a difficult financially and politically issue which it forces to carry out marginally your business and all shipping operators must maintain a sanctions screening system in place.

The last panel examined the issue of pool claims and included the following speakers Mr Ian Barr Director The London P&I Club and Mr. Dimitris Batalis General Manager Greece The Shipowners Club (SOP).

ELNAVI Newsletter

More information: ELNAVI,

19, Aristidou str., Piraeus 185 31,

Tel.: +30 210 45.22.100, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

M/T 'Alkiviadis': The 1st tanker Wind-Assisted tanker added to the fleet of Capital Ship Management

Taking advantage of all technological advances in order to reduce CO2 footprint Capital Ship Management added to its fleet the M/T “Alkiviadis” the first Wind-Assisted Ready and HVSC-Ready ABS notations and the first of six LNG fuel ready sister ships with eco-friendly design delivered to Capital in 2023.

Capital Ship Management Corp. ('Capital') took successful delivery of the newbuilding vessel M/T ‘Alkiviadis’, a 50,000 dwt, eco-type Chemical/Product MR tanker, built by Hyundai Vietnam Shipyard Co Ltd.

The HVSC-Ready notation is for vessels equipped with High Voltage Shore Connection systems to be installed in the future, and the Wind-Assist Ready notation is for vessels equipped with wind-assist equipment to be installed on board.

M/T ‘Alkiviadis’ has future proof design compliant with EEDI Phase 3 and is annotated with ABS SUSTAIN-1 (2020) that demonstrates adherence to the United Nations' (UN) Sustainable Development Goals (SDG).

Being Tier III compliant for reduced NOx emissions, assigned ABS ENVIRO notation, as well as ABS Wind-Assisted Ready, HVSC-Ready and LNG Fuel Ready notations, and equipped with IHM notation for safe recycling, the vessel becomes one of the most environmentally friendly, technologically advanced and efficient vessels in the global MR fleet.

Capital Ship Management Corp. operates a fleet of 34 tankers (12 VLCCs, 13 Aframaxes, 8 MR/Handy product tankers and 1 small tanker) with a total dwt of 5.59 million tons approx. Capital has extensive experience in managing various vessel types and sizes including all tanker segments (VLCC, Suezmax, Aframax/LR2, Panamax/LR1, MR/Handy and small tankers), dry bulk segments (Cape, Panamax, Handymax and Handy), as well as OBOs and containers.

ELNAVI Newsletter

More information: ELNAVI,

19, Aristidou str., Piraeus 185 31,

Tel.: +30 210 45.22.100, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

DNV welcomed the key stakeholders of the Greek shipping community to share insights on the latest industry trends and debate how the global socioeconomic transformations affect the shipping market.

Fifty-five guests attended DNV’s Greek Technical Committee (GTC) last December in Athens. The event, the second GTC for 2022, chaired by Mr Stavros Hatzigrigoris, came in the form of a debate. Meaningful discussions took place during the meetings of the three workgroups, and the participants raised to-the-point comments for consideration. The coordinators of each group presented in the plenum the key takeaways concerning the current requirements and challenges that the maritime industry is facing at an international level.

Decarbonization and new technologies concerns

Working Group (WG) 1 discussed Decarbonization, including the revised GHG strategy, CII and practicalities, MBM, the impact of EU’s different regulatory requirements, bio-fuels, etc.

This session was coordinated by Mr Stavros Hatzigrigoris, Chairman of the GTC and Mr Jason Stefanatos, Regional Decarbonization Director, DNV Maritime.

“For me, it was clear that apart from the EEDI/EEXI part of the forthcoming regulations, there is a lot of work to be done regarding the technology related to new fuels, decarbonization and carbon capture,” said Mr Hatzigrigoris. “The only available and tested to various degrees technologies for new fuels are LNG (leaving the methane slip aside), LPG and methanol. Availability and infrastructure continue to appear to be far behind the wishful thinking schedule. The discussion on new ship designs (possibly larger and slower ships) seems to be a kind of taboo for the industry. The reasons for this have to be further discussed and explained,” he concluded.

Need for an ESG culture that aligns with regulatory and societal demands

The topic of WG2 was Sustainability and ESG. Among the points discussed were the stakeholders and their requirements (charterers, cargo owners, financers, insurers, media, employees) and how to address them, industry standards, economic/ environmental/ social/ governance challenges, etc.

This session was led by Mr Sokratis Dimakopoulos, Chief Operating Officer, Minerva Marine Inc. and Vice Chairman of the GTC, and Mrs Chara Georgopoulou, Head of R&D and Advisory, DNV Maritime.

“We had a very interesting discussion, and an active engagement on the issue of Sustainability/Environmental, Social and Governance (ESG) and on how shipping is affected, and also on the risks/main challenges that shipping companies are facing related to ESG,” Mr Sokratis Dimakopoulos commented. “As it was widely acknowledged, due to the set decarbonization goals, the shipping industry is currently experiencing increased attention towards ESG from multiple stakeholders like Charterers, Cargo owners, Financers, Insurers, Media, etc., who require a transparent and fact-based/structured disclosure by the shipping companies of their sustainability policies/targets/ performance. Risks related to societal and environmental aspects and the need for an ESG culture were identified as highly important for ESG reporting. It was noted that several of the members of the Technical Committee have already started issuing their ESG annual reports which are prepared in accordance with applicable standards such as Global Reporting Initiative (GRI) and Sustainability Accounting Standards Board (SASB). However, the WG members noted that there could be a risk of duplication, increased administrative burden, use of additional resources and as such further work is needed in this area to ensure harmonization of applicable reporting requirements and KPIs.”

A holistic approach to the environmental footprint should be adopted

WG3 reflected on the current Energy crisis & Shipping. Mr Vassilis Lampropoulos, Chief Operating Officer, Thenamaris (Ships Management) Inc. and Vice Chairman of the GTC, and Prof. George Dimopoulos, Consultant, DNV Maritime, led the discussions concerning the impact of the energy crisis affecting the market and driving the regional developments. The group reflected on its consequences on various shipping segments, how technologies and fuels evolve, the opportunities and challenges ahead, and safety concerns.

“During our group’s discussions, it was very clear that the Energy landscape is changing and is changing fast,” commented Mr. Lampropoulos. “These changes are driven by several factors – the ambition to aggressively reduce the GHG footprint and eventually become net 0, the geopolitical and technological developments, the increasing dependency on energy, the need to find viable energy sources and carriers, as well the increased energy costs and the emerging energy trades.

Shipping, either as an energy consumer or an energy carrier, must adapt in a very tight timeframe with significant uncertainties. The path to a Clean, Affordable, Safe, Practical and Available energy solution, remains very hazy.”

Mr Lampropoulos summarized the key takeaways of the discussion: For a successful outcome, vessels and shipping should be approached in an integrated manner, not in isolation. The integration and interaction with shore and terminals should be assessed and planned together.

- A holistic approach to the environmental footprint should be adopted as early as possible to ensure a viable path without overturns on implementation. Late discussions on “fuel well to wake footprint” and delayed recognition of the distorted rating the CII offers on the efficient use of vessels are typical examples which should be avoided.

- Given the very tight timeframe a natural selection process \ approach might not be suitable this time. A more prescriptive approach, targeting specific solutions might help avoid delays, create a solid plan and secure a better outcome.

- The increasing complexity on board the vessels through the introduction of more and complex systems brings the requirement of specialized knowledge and significant time from the crew on board to operate. This can potentially distract the crew on board shift the focus and potentially lead to unsafe conditions.

- Finally, the energy costs will continue to increase and thus efficient use of energy on board the vessels will keep being high on our agenda and adopting energy-efficient designs and devices should expand.

About DNV

We are the independent expert in risk management and quality assurance. Driven by our purpose, to safeguard life, property and the environment, we empower our customers and their stakeholders with facts and reliable insights so that critical decisions can be made with confidence. As a trusted voice for many of the world’s most successful organizations, we use our knowledge to advance safety and performance, set industry benchmarks, and inspire and invent solutions to tackle global transformations.

DNV in the maritime industry

DNV is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. For more information visit: www.dnv.com/maritime

ELNAVI Newsletter

More information: ELNAVI,

19, Aristidou str., Piraeus 185 31,

Tel.: +30 210 45.22.100, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

the term ‘Green Finance’, came to my attention about two years ago, that caught me by surprise. At the time, I couldn’t realise, what it was all about exactly, what was behind of it, what was aiming at. Today, after some research on the jargon, I can understand that ‘Green Finance’ is interlinked with the Poseidon Principles (PP) adopted by the banks, and the insurance companies, to reflect the environmental impact which will be measurable as of this year through the CII requirements (Carbon Intensity Indicator) and will apply to all shipping companies. Managing risks is part of MARASCO’s every day role in Marine Insurance business. Shipping community is again called to confront new challenges. Shipping is a capital intensive business and ‘Green Finance’ could critically affect borrowers banking eligibility and their insurability.

In short, capital markets, leasing companies and banks will seriously consider the ‘green rate’ an applicant shipping company has been given, according to its ‘green footprint’ and to its CII rating, as per Poseidon Principles for Banks. PP reporting as a tool, to evaluate corporations and determine future financial performance is a possible scenario, from what we can deduce. Borrowing companies with poor decarbonization rate might encounter difficulties in the near future to access debt finance, or funding from financial institutions and consequently, might have troubles to expand, renew their fleet and eventually, as banking and insurance go hand in hand, might face some unpleasant reactions in terms and premium rates from Hull and P&I underwriters, who have adopted the Poseidon principles for Marine Insurance.

Charterers, are also getting aligned to the same direction and adopt the Sea Cargo Charter for reporting environmental pollutants. A new mindset in shipping industry is gaining slowly but surely momentum. Both, Greek and Cypriot shipping communities, have to acknowledge the coming changes, new regulations, new technologies and new challenges, if one wanted to be still competitive, not left behind, or still, to survive. PP, part of Corporate Sustainability, is not just a new trend but a necessity to comply with for any company to remain antagonistic. It could be a key element to get access to better finance, to get charterers and insurers preference – expressed in better hire and better premium - or possibly, their approval. Shipowners/Ship managers with poor green footprint rate might be viewed as substandard companies by Charterers, Banks, Insurance companies and P&I Clubs. PP mainly is used by a company for measuring the sustainability and ethical impact of an investment on a business, according to Market Business News (MBN).

The market accelerates in favor of those companies who adopt Sustainability and ESG, grapple with decarbonization of shipping early, however on the other hand, all those who cannot adopt themselves to the new, will eventually get set aside and will be extinct, as we have witnessed several times in the past. Big players and companies listed in NYSE already are in alignment with the new tendencies of the market, they follow through, but the small, medium size owner / ship manager, will possibly encounter difficulties in their efforts to adjust in many areas, including human resourcing. Sustainability, ESG (Environmental Risk, Social Risk and Governance Risk) and PP as everything else have their effects and side effects to shipowners and ship managers. The clock is ticking and we should be proactive, be open to new co operations and face challenges and threats through strategic alliances which would add value to our companies and ourselves. Marasco Marine is in contact with almost all major institutions for offering its timely assistance to its esteemed clientele, providing them proactively the right information, as decisions have to be made and better decisions are made when the right information is provided, at the right time.

-----------------------------------------------------------------------------------------------

Marasco Marine Ltd is specializing the last 31 years in Marine Insurance/Risk Management and Marine Insurance Claims for ocean going, commercial vessels over 5,000 DWT. More at: www.marasco-marine.com

ELNAVI Newsletter

More information: ELNAVI,

19, Aristidou str., Piraeus 185 31,

Tel.: +30 210 45.22.100, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

The 7th Posidonia Sea Tourism Forum (PSTF) to examine region’s growth opportunities from lucrative tourism segment

The appeal of Greece and the East Mediterranean as an ideal region for luxury cruising will be one of the main highlights of the 7th Posidonia Sea Tourism Forum (PSTF), scheduled to take place in Thessaloniki on the 25th and 26th of April, 2023.

Luxury and niche cruise brands that have already confirmed participation for the two-day event to be held at Thessaloniki’s landmark five-star hotel Makedonia Palace include Azamara Cruises, Compagnie du Ponant, Scenic Cruises, Seabourn Cruise Line, Variety Cruises and recently re-launched Crystal Cruises.

Delegates and exhibitors from around the world will have the chance to attend a panel discussion titled: ‘The Appeal of Venturing to Non-Mainstream Destinations: Luxury & Expedition Cruising leading the Way’ that will examine the increasing importance of lesser-known destinations for this specific market segment, in conjunction with infrastructure challenges and the role of sustainability and authenticity as desirability factors.

“Our decision to move the Posidonia Sea Tourism Forum away from Athens for the first time in the event’s 12-year-long history was in sync with emerging trends in an industry that wishes to constructively address growing criticism for its contribution to over-tourism in many cruise hotspots around the world,” said Theodore Vokos, Managing Director of Posidonia Exhibitions S.A.

“Thessaloniki was chosen as the host of this year’s event to signify the need for more port alternatives and new destinations to dilute impact and optimise cruise traffic management in the East Mediterranean region. Also, Thessaloniki is a natural gateway for emerging Balkan markets, which is another important topic to be addressed during the Forum.”

With more than 400 inhabited islands and coastal cities across Italy, Croatia, Greece, Albania and Turkey, the East Mediterranean and Adriatic seas collectively offer one of the highest densities of destination alternatives in the world. There are countless potential new ports-of-call, as well as main and regional homeporting options beyond the well-established marquee destinations.

Diverting some traffic from over-frequented destinations will enrich the itinerary design menu, as well as act as a tool that can protect the natural, cultural and tourism values needed for a sustainable future.

Mark Robinson, Senior Vice President Operations, Scenic Luxury Cruises & Tours, said: “The luxury cruise segment represents 3.7% of the industry’s total market share worldwide, with the Mediterranean Sea owning over a third of that with 37.01%. One of the main drivers for the region’s appeal is the East Med archipelago which offers unique, famous worldwide destinations and hidden gems which offer ultimate customisation destination services. With our Scenic and Emerald Cruise luxury yachts we have many calls in the region, and we are happy to announce that in 2023 our new ultra-luxury expedition yacht Scenic Eclipse II, due to be launched in April, and our new Emerald Sakara yacht will debut in the East Med Region in July. Scenic Cruises is always looking for new destinations for our luxury cruises, and the East Med has many hidden gems for us to tap into with its rich heritage, friendly locals and not to mention the excellent cuisine and turquoise blue seas.”

Some 85 luxury vessels totalling 36,184 berths will be operating cruises this year. This represents an annual capacity of 1,050,000 passengers and the prediction for 2027 is up to 94 ships totalling 44,764 berths and 1,378,000 passengers.

“According to the Allied Market Research Report, Greece’s luxury tourism offering is expected to yield an annual revenue of USD 2,7 billion by 2030, registering a CAGR (Compound Annual Growth Rate) of 11.5% from 2021 to 2030. A significant part of this revenue will come from luxury cruise activity and on-shore spending from this segment’s high-income passengers,” added Vokos.

Luxury cruise passengers seek a wide range of unusual, often specialized and certainly more immersive destination experiences and are prepared to pay a premium to satisfy their expectations. Greece and the East Mediterranean are gifted with a level of destination diversity that can satisfy even the most highly demanding expectations of today’s discerning travellers.

Other interesting topics to be discussed during PSTF 2023 will include the long-term prospects for the cruise industry as an important sector of the leisure travel market and the necessity for regions and cruise lines to cooperate on the enhancement of destination offerings, on the upgrading of infrastructures, on the popularization of alternative ports of call and finally, on improvements of cruise traffic management aimed at defusing over-tourism.

The 2023 PSTF is sponsored by Diamond Sponsor Thessaloniki Port Authority S.A., Silver Sponsor Piraeus Port Authority SA, Bronze Sponsors Celestyal Cruises, Global Ports Holding and Kyvernitis Travel. It is organised under the auspices of the Ministry of Maritime Affairs & Insular Policy and the Ministry of Tourism and supported by the Hellenic Chamber of Shipping, the Cruise Lines International Association (CLIA), the Association of Mediterranean Cruise Ports (MedCruise) and the Union of Cruise Ship Owners & Associated Members.

ELNAVI Newsletter

More information: ELNAVI,

19, Aristidou str., Piraeus 185 31,

Tel.: +30 210 45.22.100, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Hellenic Hull, as a founding member of the Poseidon Principles for Marine Insurance is among the world’s leading marine insurers that have published client data to track their hull and machinery insurance portfolio’s climate impact. The goal is to support the industry’s green transition.

The first Annual Disclosure Report for Poseidon Principles for Marine Insurance is a landmark step forward towards transparency in the maritime and insurance sectors. The data will act as a stepping-stone for the Signatories to engage their clients in a discussion about climate change, technology, and new risks.

“This level of transparency is a major milestone on our journey to decarbonise the maritime industry,” says Patrizia Kern, Chair of the Poseidon Principles for Marine Insurance initiative and Marine Strategy Advisor – CEO Office at Swiss Re Corporate Solutions. On average, the Signatories’ portfolios are 12.7% above being aligned with reaching the UN maritime-goal of at least 50% reductions of the annual greenhouse gas emissions from international shipping by 2050, compared with their level in 2008. The second trajectory the Signatories track takes is more ambitious and has a goal of zero CO2 emissions in the middle of this century. The simple average score of the 100% CO2 emission reduction track is 20.8% above alignment. “It is evident that there is work to do, but hard data and transparency is a necessary first step,” Kern says.

“Transparency is our utmost priority in every aspect of our business activities. Our first climate alignment score indicates that we should work together with our clients to assist them in this transition. The knowledge acquired in the reporting process enabled us to analyze these results with the aim of fine-tuning our sustainability strategy. As mentioned in the report, our portfolio needs improvement with regard to IMO & 100% CO2 reduction trajectories. Following an open data policy, we are committed to share the data with our clients and launch an open dialogue on how to eliminate the climate related risks of our portfolio, providing a roadmap to our clients to meet climate efficiency of their fleet,” underlines Ilias Tsakiris, CEO of Hellenic Hull and Chairman of the Ocean Hull Committee of the International Union of Marine Insurance.

Gathering data on the portfolios is a complex task. First of all, readers should take note that the data covers 2021 – not 2022. Further, the numbers do not cover the Signatories’ entire hull and machinery portfolios, as not all clients reported their data back to the insurance providers. In addition, it is industry practice that each ship is insured by a primary insurer and several secondary insurers, because of the extraordinary value of modern ships, which adds another level of complexity to the data collection.

Many takeaways

Read the report for a full breakdown of methodology and individual responses here 2023 ambition

The Poseidon Principles were established in 2019 by the Global Maritime Forum and a number of financial institutions to create a global framework to quantitatively assess and disclose whether financial institutions’ lending portfolios are in line with climate goals. In addition to the annual report on Marine Insurance, the Poseidon Principles for Financial Institutions published their third annual disclosure report with 28 of them reporting in December 2022. For 2023, the ambition of the Poseidon Principles for Marine Insurance is to get more members to join the principles, increase the contribution volume from the insurance clients and improve access to data.

Industry foundation is shifting

The very foundation of the maritime insurance sector is changing, according to the Signatories, because the maritime industry has begun its transition away from the monolithic oil-based combustion technology towards a future with a wide array of propulsion technologies and energy sources. Therefore, each company within the marine insurance sector must understand what they will insure in the future and how new ship technology will work.

“The insurance companies are only one component in a complex ecosystem, but while engaging with our clients we can become levers of change,” Kern says.

Climate change is a ‘here and now challenge’ for the global insurance industry, and the marine insurers see their engagement with their clients as a way of contributing to the wider sector, given that international shipping emits 2-3 percent of global greenhouse gas emissions, transporting close to 80 percent of global trade by volume.

Reporting Signatories:

Fidelis MGU, Gard, Hellenic Hull Management, Navium, Norwegian Hull Club, SCOR, Swiss Re Corporate Solutions and Victor Insurance.

Affiliate members: Cambiaso Risso Group, Cefor, Cosco Shipping Captive, CTX Special Risks, EF Marine, Gallagher, Lochain Patrick Insurance Brokers, Lockton Marine, WTW.

About the Poseidon Principles for Marine Insurance

The Poseidon Principles for Marine Insurance are a framework for measuring and reporting the alignment of insurers’ shipping portfolios with climate goals. Recognising insurers’ role in promoting responsible environmental stewardship throughout the maritime value chain, the Poseidon Principles for Marine Insurance provide them with tools to foster collaboration with clients, gain insight to enhance strategic decision-making, and address the impacts of climate change. The Annual Disclosure Report 2022 was produced by the Global Maritime Forum, which performs secretariat services for the Poseidon Principles for Marine Insurance, with expert support provided by UMAS and Swiss Re Institute. The Poseidon Principles for Marine Insurance are built on four principles – Assessment of climate alignment, Accountability, Enforcement, and Transparency – which they share with the Poseidon Principles for Financial Institutions and the Sea Cargo Charter. Established under the auspices of the Global Maritime Forum, the three initiatives aim to increase the transparency of environmental impacts within global seaborne trade, promote industry-wide change, and support a better future for the industry and society.

For more information, please visit www.poseidonprinciples.org/insurance

ELNAVI Newsletter

More information: ELNAVI,

19, Aristidou str., Piraeus 185 31,

Tel.: +30 210 45.22.100, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

The third meeting of the Hellenic Decarbonization Committee (HDC) was held at the end of the year. The committee was set up to give a vital discussion forum to shipowners and other stakeholders on the way forward to meet decarbonization targets. From the start of 2023 each ship will require an approved Ship Energy Efficiency Management Plan (SEEMP) on board and the Carbon Intensity Indicator (CII) regulation will come into force. The impact of both were key focusses for the attendees.

Shipping will remain the core means of transport for decades to come and, as pointed out by RINA Deputy Marine Operations Executive Vice President, Massimo Volta: “Decarbonization is not a theoretical exercise. We need feasible solutions in line with the feedback from shipowners, in respect to both the environment and the people involved.”

The HDC is formed of key stakeholders in the Greek shipping industry and is chaired by Ioanna Procopiou, CEO of Sea Traders and founder of Prominence Maritime. During the opening session of the HDC, she said: “Alternative fuels will not be the dominant solution during the transition period. We will need to look to other solutions, including carbon capture.”

Ms. Procopiou’s comments reflect the fact that decarbonization will be a long process. We do not have all the answers today and need to move forward with practical, ‘doable’ solutions that will reduce shipping’s carbon footprint, while we strive for net zero in the future. This makes the HDC a vital forum to progress with decarbonization at the pace needed to meet IMO targets in the future.

The shipping industry is already embracing increasing regulations that are aimed at reducing environmental impact. In 2023, ships will be subject to both Energy Efficiency Existing Ship Index (EEXI) and CII regulations. While EEXI is specific to a particular vessel, the CII rating will mainly depend on the ship’s operations. Factors that will affect a ship’s CII performance will include operational aspects such as sailing speed, engine running hours, and the prevailing ambient conditions at sea.

Giosuè Vezzuto, Executive Vice President Marine at RINA concluded: “We do not know what fuels or technologies will become winning options for the future, but we need to develop now if we are going to meet targets in the future. The industry cannot stand still and, indeed, as a class society, neither can (we at) RINA. We are working proactively to support the transition and facilitate approaches to safety and risk assessments as we wait for prescriptive rules to follow developments”.

The HDC discussed several solutions that will assist existing vessels with CII compliance, something which many will have difficulties with to begin with. However, through a combination of technical modifications, it was proposed that vessels could improve their fuel consumption by up to 20%. A roadmap, detailing discrete actions for both retrofitting existing vessels and new builds was also presented at the meeting, looking from the situation today to 2050 and beyond.

The HDC had previously established four working groups covering: EU ETS and FuelEU Maritime, IMO EEXI, IMO CII & Operational Profiles, and Alternative Fuels. These groups look to provide practical answers to the challenges faced by shipowners, today and into the future. They will work to provide calculation costs when the final drafts of both the ETS directive and Fuel EU Maritime Regulation become available and examine EEXI implementation issues and any adaptation of CII calculations that may be needed as we learn about the impact of this regulation. While the Alternative Fuels working group has already successfully carried out a study for the application of LNG Reforming with Carbon Capture, its next focus will be more specifically on carbon capture technologies.

The HDC will meet again in a few months’ time to discuss further progress of the working groups and to continue its efforts to find practical solutions that will take the shipping industry on a sustainable and viable path towards net zero.

Members of the Hellenic Decarbonisation Committee:

Ioanna Procopiou, Owner Prominence; George Procopiou, Owner Dynacom; George Youroukos, Owner Technomar; Andreas Hadjigiannis, Owner Cyprus Sea Lines; Andreas Martinos, Owner Minerva; John Mytilinaios, Owner M Maritime; Nikolas Martinos, Owner Thenamaris; Harry Vafias, Owner Stealth; Stathis Topouzoglou, co – CEO Prime; Michael Halkias, co – CEO Prime; Konstantinos Krontiras, Owner Roxana Shipping; Nicole Mylona, Owner Transmed; Suzanna Laskaridis, Owner Laskaridis Shipping; Stamatis Tsantanis CEO Seanergy; George Mangos, Principal Interunity; Christos Mangos Principal Interunity; Loukas Sigalas, Managing Director Minoan Lines; Spyros Paschalis CEO Attica Group; Mathios Rigas, CEO Energean; Panos Kourkountis, Technical Manager SeaTraders; Theodore Baltatzis, General Manager Technomar; Tom Lister, CCO Global Ship Lease; Sokratis Dimakopoulos, COO Minerva; George Christopoulos, COO Laskaridis Shipping; Takis Koutris, General Manager Roxana Shipping; Nikolas Tamichiakis, Technical Manger Minoan Lines; George Daskalakis, Deputy CCO M Maritime; Petros Tripolitis, Technical Manager M Maritime and George Anagnostou, COO Attica Group.

image1: Mrs. Ioanna Procopiou, CEO of Sea Traders and founder of Prominence Maritime

image 2: Mr. Massimo Volta, RINA Deputy Marine Operations Executive Vice President

image 3: Giosuè Vezzuto, Executive Vice President Marine at RINA

ELNAVI Newsletter

Περισσότερες πληροφορίες : ELNAVI,

Αριστείδου 19, Πειραιάς 18531,

Tel.: +30 210 45.22.100, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Charalambos Fafalios: “Greek shipping in renewal and expansion mode despite the turbulent global environment”

On the occasion of GSCC vassilopitta (New Year’s pitta) the chairman Mr. Charalambos Fafalios, referred to the latest shipping and geopolitical developments described the current conditions in each shipping sector and expressed his expectations for the New Year.

Last year Ukraine has become a war zone and the effects of this conflict have been more far reaching than we would have ever imagined.

All of a sudden, commodity prices rose briskly, supply routes changed and trade patterns have altered to a degree that we would not have envisaged.

The result has been positive for some sectors of shipping and negative for others. If we look at dry commodities Ukraine was mostly a very short haul exporter therefore replacing their grain and coal exports has had a very beneficial effect on tonne miles. The resulting sanctions on Russian exports such as oil and gas have also been very positive for the tanker and gas carrier markets.

However, we should never forget the sad consequences for the citizens of Ukraine who are living through this unnecessary conflict with great loss of life.

World shipping has to navigate in this global environment whilst at the same time trying to reduce its carbon footprint appreciably.

It must never be forgotten that shipping has always made a virtue of creating ever more energy efficient ships and reducing its fuel footprint per tonne of cargo carried.

The issue of what future propulsion method will be adopted or what fuel is chosen, is still anything but settled as an issue.We are still awaiting engine and ship builders to come up with real green solutions.

It is very important to stress that we support the IMO exclusively and not the many regional markets because we need global solutions and not regional efforts.

In the short term, we must be patient and realise the real benefits of EEXI. The operational index, CII, another short-term measure in the IMO roadmap seems to have no respect from either charterers or shipowners. World shipping is too complex to try and use rather simplistic measures for vessels fuel efficiency.

Looking back over the last 12 months, the fates of various shipping sectors have almost been a rollercoaster ride. The container market, which saw the highest freight rates ever last year, is now languishing at levels which are 80-90 percent below their peaks and with a disturbingly large order book. The tanker market rose from the doldrums and even now various sectors are performing very well. The LNG / LPG markets also have seen some historically high freight rates and the order book has risen to very high levels. The car carrier sector has also risen from its pandemic level lows and is rewarding its owners well at the moment. The dry bulk market, which started 2022 strongly is now at rather disappointing levels and it is uncertain as to what may bring about a turnaround. Its fleet is the largest on record and the orderbook although historically low is certainly not negligible.

Against this background, the Greek controlled merchant fleet, amongst the largest in the world, is getting younger by the year due to judicious second-hand sales and a substantial orderbook of low carbon high technology newbuildings in all sectors.

We still urge the Greek government to improve the maritime education system and allow more private education establishments. If bureaucracy is greatly reduced, the Greek flag itself will benefit.

Through conflicts, pandemics, bad weather and difficult circumstances, the men and women who are part the shipping industry including our seafarers are the unsung heroes that make world trade possible and so positively impact our way of life. Governments should enshrine this status with deeds and not only with words!

ELNAVI Newsletter

More information: ELNAVI,

19, Aristidou str., Piraeus 185 31,

Tel.: +30 210 45.22.100, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.