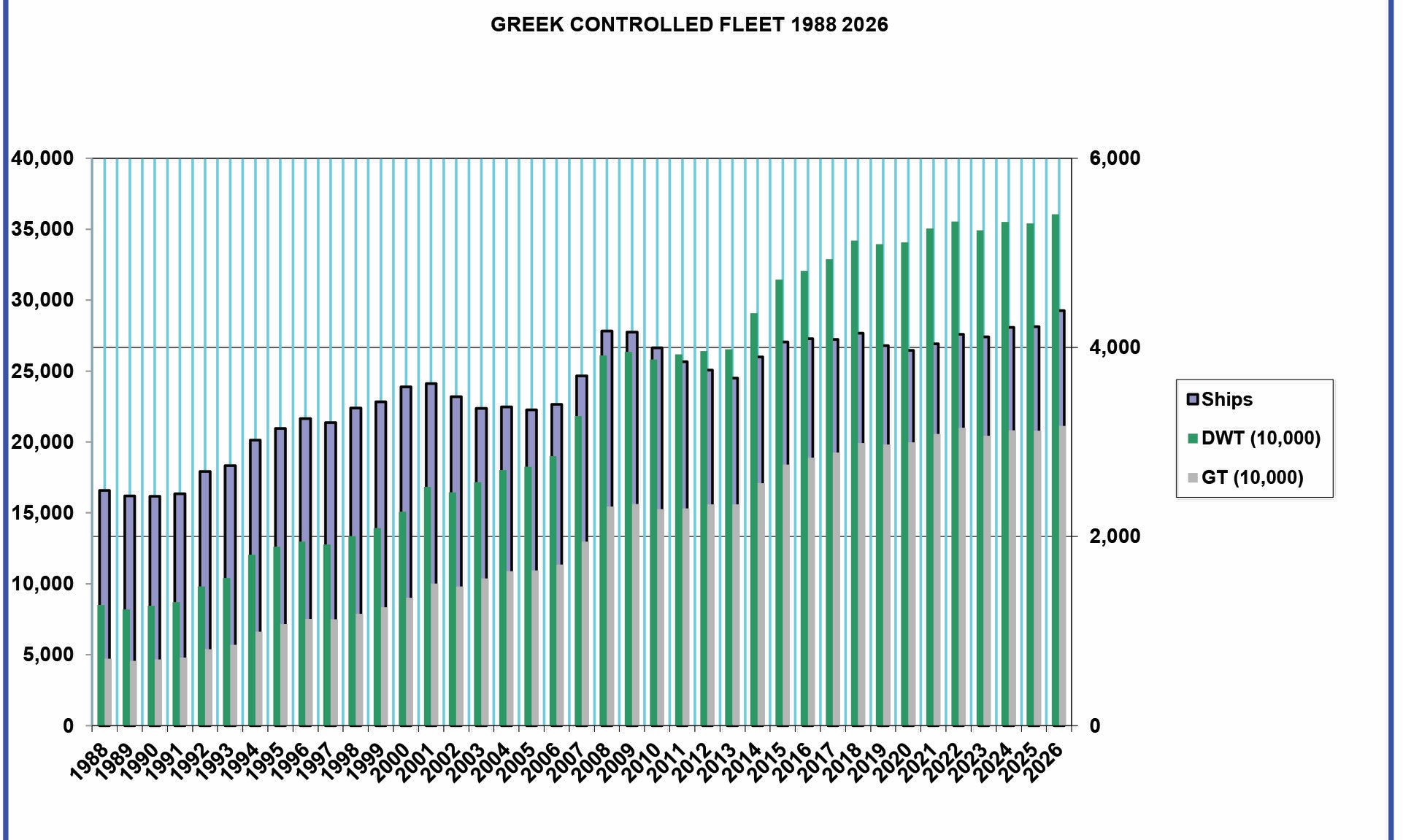

Greek-controlled fleet has reached an all-time high, reinforcing Greece’s position as a global maritime superpower. Despite regulatory shifts and flag competition, the fleet saw significant year-over-year growth in every primary metric.

The Total Controlled Fleet stands at 4,388 vessels (+167 YoY), Total Deadweight Tonnage (DWT) 360,564,729 (+6.4M YoY), Total Gross Tonnage (GT): 211,204,583 (+3.1M YoY) and the Future Pipeline includes 422 vessels currently on order (40.2M DWT).

Flag State Analysis

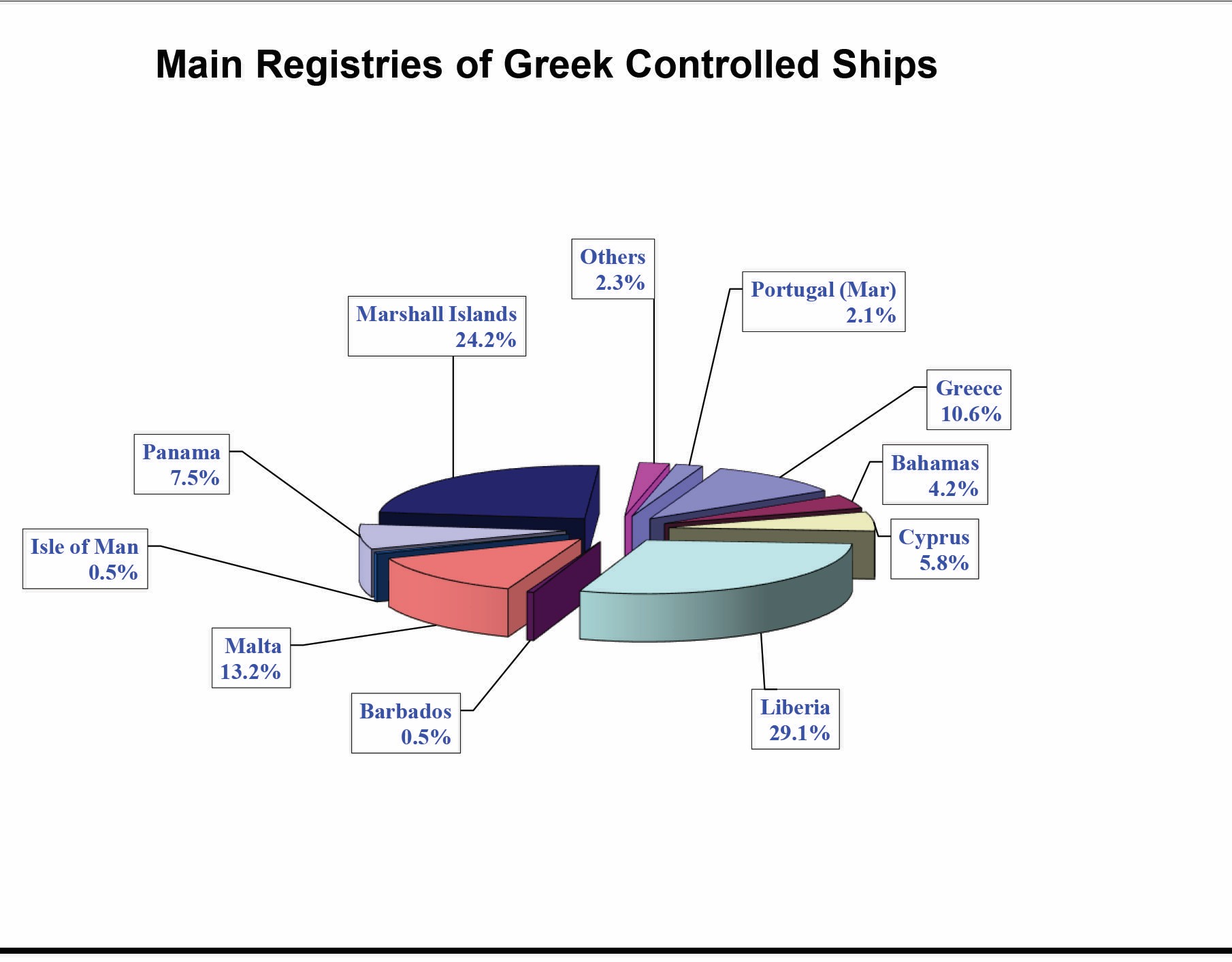

The Greek-controlled fleet is diversified across 31 international flags. While the Greek national registry remains a top-tier global player, there is a clear trend toward "Open Registries" like Liberia and the Marshall Islands, which offer greater administrative flexibility.

Liberia gained a record number of 130 vessels, Panama gained 30 ships, Marshall Islands gained 25 and Portugal (Madeira) 19. The Cyprus and Barbados registry remained unvaried in terms of number of vessels.

The number of vessels registered under the Greek flag decreased slightly this year by 17 vessels. In terms of DWT and GT there was a decrease of 3,773,090 and 2,106,014 respectively.

Overall, the Liberia and Marshall Island flags are at the forefront of the Greek-owned fleet with 1,279 and 1,061 Greek-owned ships, respectively, on their registers. In terms of DWT, Liberia accounts for 111,307,219, representing 30.1%, Marshall Islands accounts for 83,286,472, representing 23.1 % and Malta with 579 ships of 50,891,381 DWT, representing 14,1% of the total DWT of the Greek-owned fleet. The Greek flag stands with 463 ships of 44,944,717 DWT. It should be noted that the Greek flag remains in the fourth place globally in terms of DWT, as it represents 12.5% of the total DWT of the Greek-owned fleet.

In terms of DWT, Panama follows with 330 ships of 22,728,332 DWT, Cyprus with 253 ships of 19,024,790 DWT and Bahamas with 183 ships of 15,536,597 DWT. Furthermore, it should be noted that the total number of vessels registered under EU flags stands at 1,388, which accounts for 31,6% of the Greek fleet. This figure has decreased, when compared to the previous year’s figure of 1,414 vessels, which represented 33,5% of the Greek fleet.

Market Share & Sector Specialization

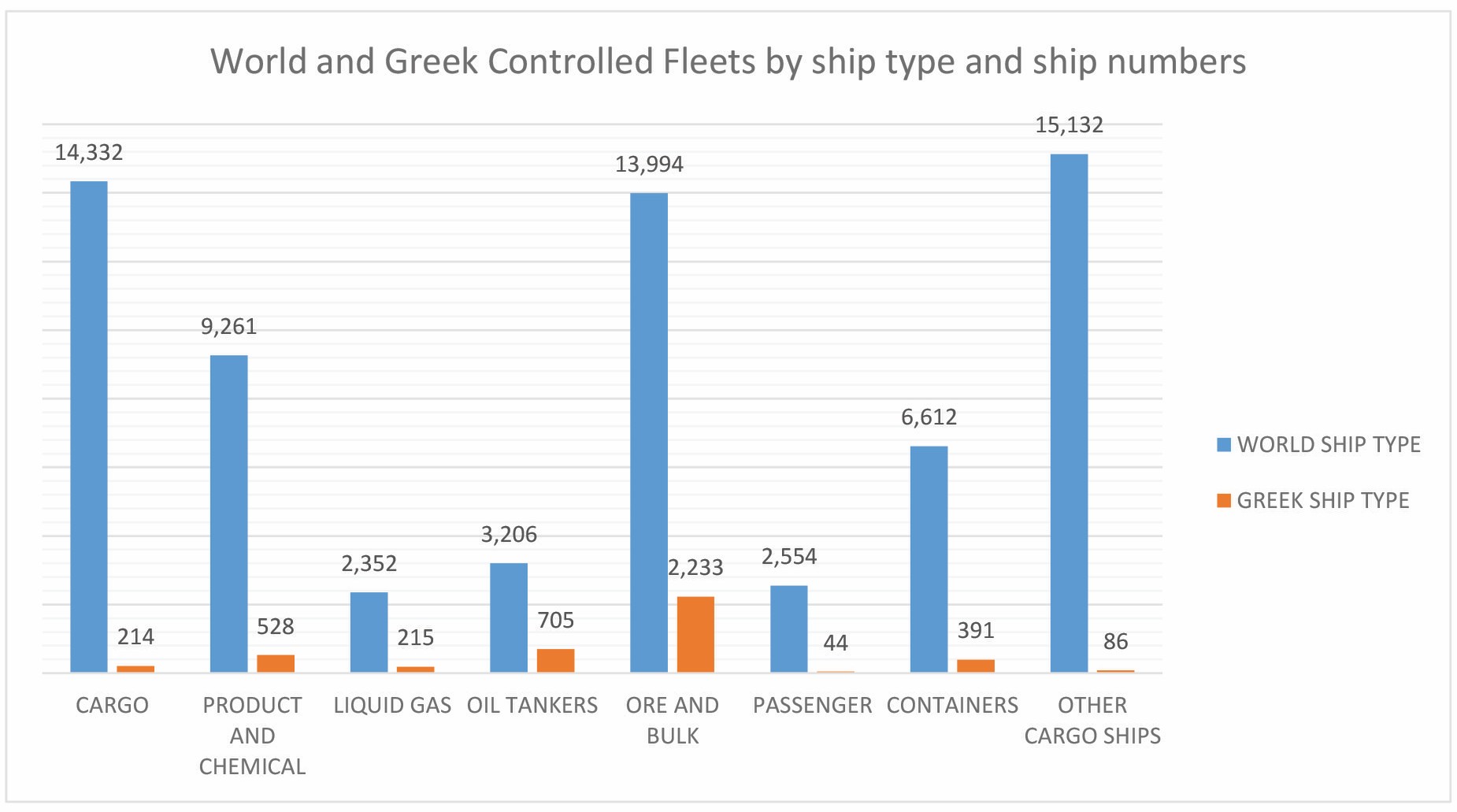

Greek shipping remains the backbone of global energy and bulk trade. The Greek fleet's footprint is significantly larger than its "vessel count" suggests because Greek owners tend to operate larger, high-capacity ships.

Greek Share of the Global Market

- • World Tanker Fleet: 22% (by capacity)

- • World Ore & Bulk Fleet: 16%

- • World Liquefied Gas Fleet: 8%

- • Total World Fleet (DWT): 14.2%

Current Order Book (Newbuilds)

The 422 vessels on order reflect a strategic pivot toward liquid bulk and specialized transport:

- • Oil & Product/Chemical Tankers: 201 vessels

- • Ore & Bulk Carriers: 77 vessels

- • Container Ships: 74 vessels

- • Liquefied Gas Carriers: 43 vessels

Fleet Age & Sustainability

A younger fleet is a more efficient and compliant fleet. Greek owners continue to outperform the global average in terms of vessel modernization.

The average age of the Greek-controlled fleet in terms of ships increased slightly compared to the previous year, but, nevertheless, continues to be 4.5 years below the average age of the world fleet.

The average age of the Greek controlled fleet in terms of ships now stands at 14.3 years, in comparison to 18.8 years for the world fleet. In terms of GT and DWT, it is 12.8 and 12.7 years respectively, as against 13.8 and 13.7 of the world fleet.

The average age of the existing Greek flag fleet recorded a slight increase in terms of ship numbers, now standing at 16.6 years, in comparison to 16.3 years in 2025. A slight increase has also been noted in terms of GT and DWT, with values of 11 and 10.6 years respectively, as against 10.7 and 10.3 years in 2025.

Classification Societies

Greek owners rely on top-tier classification societies to ensure safety and compliance. ClassNK and Lloyd’s Register remain the preferred partners for the majority of the fleet.

- ClassNK: 891 ships

- Lloyd’s Register: 804 ships

- ABS: 757 ships

- BV: 739 ships

- DNV: 607 ships

- RINA: 352 ships

Conclusion

The Greek maritime industry has demonstrated remarkable resilience and expansion. While the shift toward non-EU flags continues due to bureaucratic pressures, the overall growth in DWT and the modern age profile of the fleet ensure that Greek shipping remains the dominant force in the global supply chain for 2026 and beyond.

ELNAVI Newsletter

More Information: ELNAVI,

19, Aristidou str., Piraeus 185 31,

Tel.: +30 210 45.22.100, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.