The Signal Ocean Voyages API offers a deep dive into global versus U.S. port calls for both dry bulk and tanker vessels, providing valuable insights into which vessel size segments and commodity types are most exposed to recent policy developments. In light of these shifts, a critical question emerges: Is the U.S. shipbuilding industry truly positioned to play a pivotal role in the freight market at this moment?

The shipbuilding industry is a critical sector for the economic and geopolitical strength of any nation, especially when it intersects with commercial shipping and maritime power. In the age of globalisation and geo-economic competition, the relationship between the United States and China in the shipbuilding domain is marked by growing tensions, particularly regarding trade policies such as the imposition of port tariffs and duties on shipbuilding products.

The recent proposal by the U.S. Trade Representative (USTR) to impose substantial port fees on Chinese-built and Chinese-operated vessels is poised to significantly impact the global freight market. The proposed fees include charges of up to $1.5 million per port call for operators using Chinese-built ships and up to $1 million per port call for Chinese maritime transport operators. Additionally, operators with existing or pending orders from Chinese shipyards may face similar fees. Implementing these fees is expected to lead to increased operational costs for shipping companies, which will likely be passed on to consumers through higher freight rates. The World Shipping Council estimates that these fees could add approximately $600–$800 per container, effectively doubling the cost of shipping U.S. exports. This escalation in shipping costs may reduce the competitiveness of U.S. exports, potentially leading to decreased trade volumes and shifts in global trade patterns.

The U.S. Shipbuilding Industry: Limited in Scope, Strategic in Value

The United States has a rich history in shipbuilding, particularly in the military and domestic commercial sectors. The Jones Act of 1920—which requires that vessels operating between U.S. ports be built in the country, owned by American entities, and crewed by U.S. citizens—has long shielded the domestic industry from foreign competition. Yet despite this protection, America’s commercial shipbuilding capacity has shrunk dramatically. Today, only a handful of shipyards remain active, hampered by high construction costs and limited global competitiveness. Nevertheless, the sector remains strategically vital, deeply intertwined with national security and supply chain resilience.

China’s Commanding Lead in Global Shipbuilding

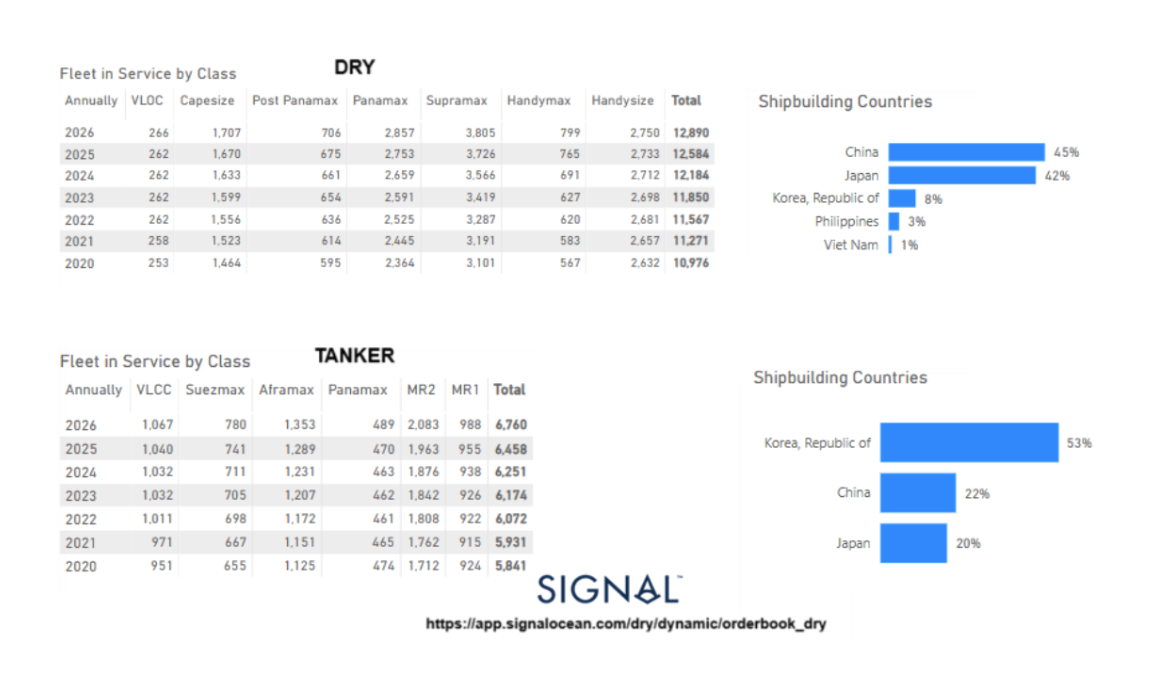

In contrast, China has emerged as the dominant force in global commercial shipbuilding, accounting for 45% of the dry bulk fleet’s newbuild orders, according to Signal Ocean data. This leadership is supported by substantial state subsidies, low labor costs, and an expansive industrial ecosystem. Chinese yards are renowned for their cost efficiency and rapid delivery times, attracting global demand—including from U.S. shipowners. Beyond hull construction, China also exports a wide array of ship components, from engines to maritime electronics, reinforcing its central role in the maritime supply chain. While Japan remains highly competitive in dry bulk construction (42%), South Korea leads the tanker segment with a 53% share—demonstrating regional specialisation and deliberate industrial policy. As of 2025, the global tanker fleet (VLCC, Suezmax, Aframax, Panamax, MR2, MR1) is approximately 6,000+ vessels. (as depicted in the image below) China accounts for 22% of the global tanker shipbuilding market, meaning roughly 1 in 5 tanker vessels in the current fleet is likely Chinese-built.

Prospects for a U.S. Shipbuilding Revival

Rebuilding the U.S. commercial shipbuilding sector presents formidable challenges. Currently, the United States accounts for just 0.13% of global commercial vessel production, while China, Japan, and South Korea together command more than 90% of the market. Further compounding this disparity, ship construction costs in the U.S. are estimated to be three to four times higher than in East Asia. Revitalising the domestic industry would demand large-scale investments in infrastructure, advanced manufacturing, and skilled labor development.

To bridge these capability gaps, strategic partnerships with established shipbuilding nations like South Korea and Japan have been suggested. However, overcoming the deeply rooted advantages of Asian competitors—bolstered by decades of industrial policy, scale, and specialisation—remains a significant hurdle.

Against this backdrop, the U.S. government is increasingly turning to geoeconomic tools such as port tariffs, signalling a broader departure from traditional free-trade principles toward a more interventionist industrial strategy. Bolstering the domestic shipbuilding base is now framed not just as an economic goal, but as a strategic imperative—central to national defense, supply chain security, and maritime sovereignty. This urgency is magnified by ongoing global instability, including the war in Ukraine and rising tensions in the Indo-Pacific.

Yet, tariffs alone will not restore America’s competitive edge in shipbuilding. Lasting progress will depend on sustained public and private investment, technological innovation, and a coordinated industrial policy that supports long-term capacity-building.

Implications for International Shipping and Global Trade

Increased tariffs on Chinese shipbuilding exports and potential port duties on Chinese-built ships could trigger significant disruptions in the global shipping system. Shipowners operating Chinese-built vessels may face higher costs to access U.S. ports, costs that are likely to be passed along the supply chain, contributing to higher transportation costs and inflationary pressures. Moreover, if China retaliates with reciprocal measures, it could restrict American companies' access to Chinese ports, leading to a realignment of trade flows and a deepening of economic decoupling between the two powers.

The Grain Impact

Increased Transportation Costs: The American Farm Bureau Federation estimates that proposed port fees could add between $372 million and $930 million in annual transportation costs for bulk agricultural exporters. This significant rise would erode the cost advantages that have traditionally helped U.S. farm products stay competitive in global markets. For example, the extra fees could increase the cost of shipping a bushel of soybeans—currently trading at $10.07—by as much as 27.75 cents. In commodities trading, where margins are razor-thin and often decided by just a few pennies per bushel, this would represent a serious blow to exporter profitability.

Reduced Export Competitiveness: As shipping costs climb, U.S. grain exporters may be forced to reduce their sale prices to remain competitive, thereby cutting into already tight profit margins. The financial strain could ultimately lower the volume of U.S. grain exports, especially as buyers shift to countries with lower transportation costs. Reports from exporters indicate that freight costs have surged by as much as 40%, making it increasingly difficult to secure bids for shipments of soybeans, corn, and wheat.

Impact on Farmers: This cost burden trickles down directly to American farmers, many of whom depend on international markets to sell their harvests. Without access to affordable freight, growers face the grim prospect of being priced out of global supply chains. The American Soybean Association has warned that these additional port fees could effectively shut U.S. soybeans out of export markets altogether, threatening the economic viability of farming operations across the Midwest and beyond.

Broader Economic Implications – Including Tanker Sectors: While the grain sector is most directly affected, the proposed port fee hikes could have ripple effects across the broader U.S. economy. The energy sector, for example, has voiced concern that rising transportation costs could undermine U.S. oil and gas exports. Tanker operators warn that increased fees may hamper efforts to solidify energy dominance by making U.S. shipments less competitive in the global marketplace. Likewise, the mining industry—another key user of bulk and tanker shipping—has flagged potential supply chain disruptions and higher export costs that could bring parts of the sector to a standstill.

Based on The Signal Ocean Voyages API data and in connection with the recent U.S. proposal to impose port fees of up to $1.5 million per call on Chinese-built ships, here's a comprehensive market impact analysis of U.S. port fees on Chinese-built vessels.

ELNAVI Newsletter

More Information: ELNAVI,

19, Aristidou str., Piraeus 185 31,

Tel.: +30 210 45.22.100, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.